Maldives Islamic Bank Ends 2025 with Strong Earnings Growth

Earnings surge 52% year-on-year, capping a year of sustained balance sheet growth

Maldives Islamic Bank Plc

Earnings surge 52% year-on-year, capping a year of sustained balance sheet growth

Maldives Islamic Bank Plc

Maldives Islamic Bank (MIB) concluded 2025 with a strong fourth quarter, as continued growth in financing activity and customer deposits supported further expansion in earnings and the balance sheet. Net profit reached MVR 100.0 million in Q4 2025, rising 8.3% from the previous quarter and 52.1% compared to the same period last year, while total assets expanded sharply alongside strong deposit mobilization. Despite the rapid growth, the Bank maintained comfortable liquidity and solid capital buffers, with capital adequacy improving to 16.2%. Operationally, the Bank continued expanding its digital banking footprint during the year, supported by rising usage of digital platforms and increasing electronic transaction volumes. These developments took place against a supportive macroeconomic backdrop, with strong tourism activity and continued expansion in private sector credit sustaining favorable conditions for banking sector growth.

Overall, the Bank’s continued earnings momentum and balance sheet expansion, together with strong profitability reflected in a return on equity above 28%, suggest that the Bank remains well positioned for further growth. At around 1.7x book value and 6.5x earnings, the current valuation also appears modest relative to the Bank’s underlying earnings strength and return profile.

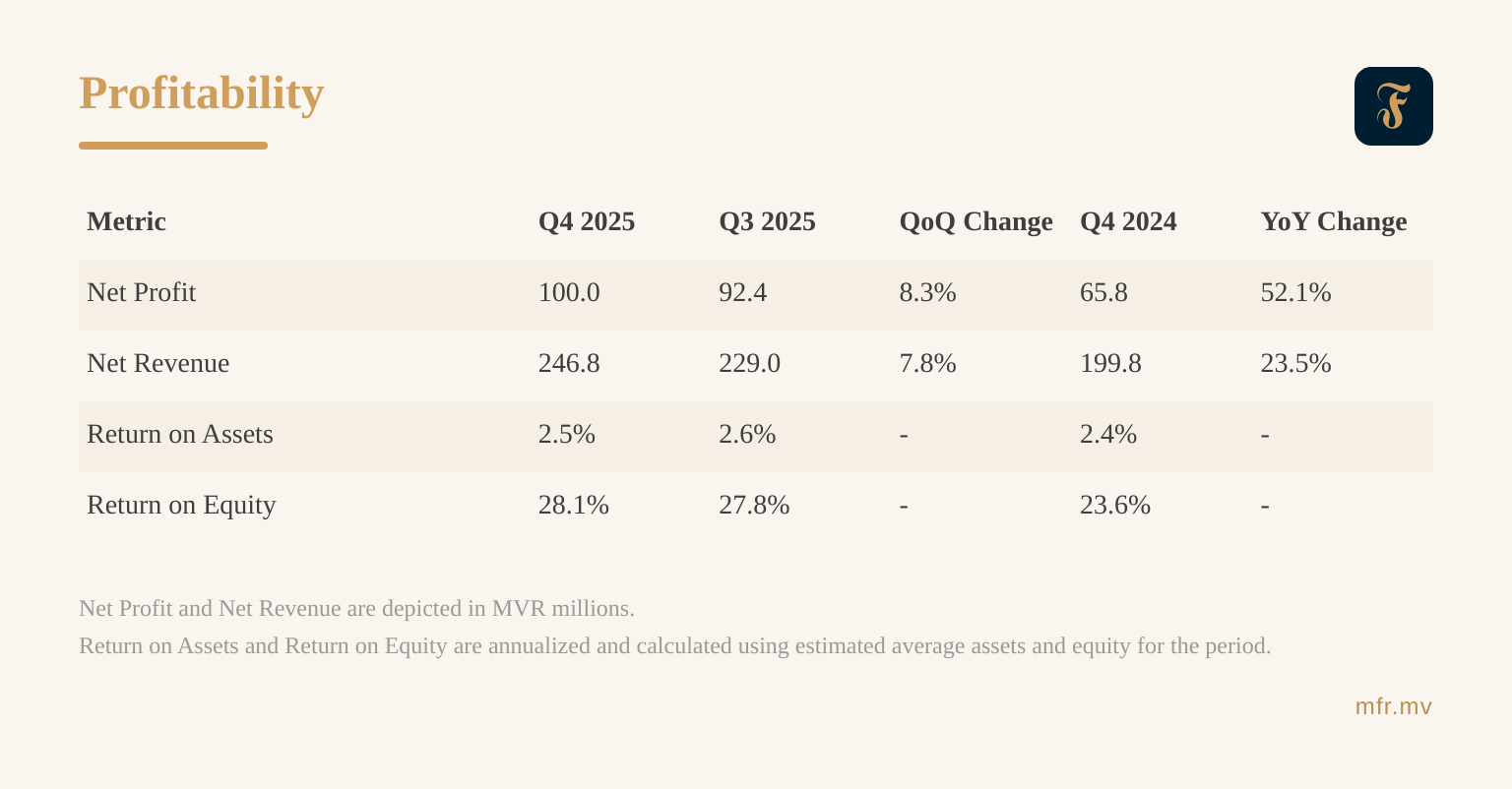

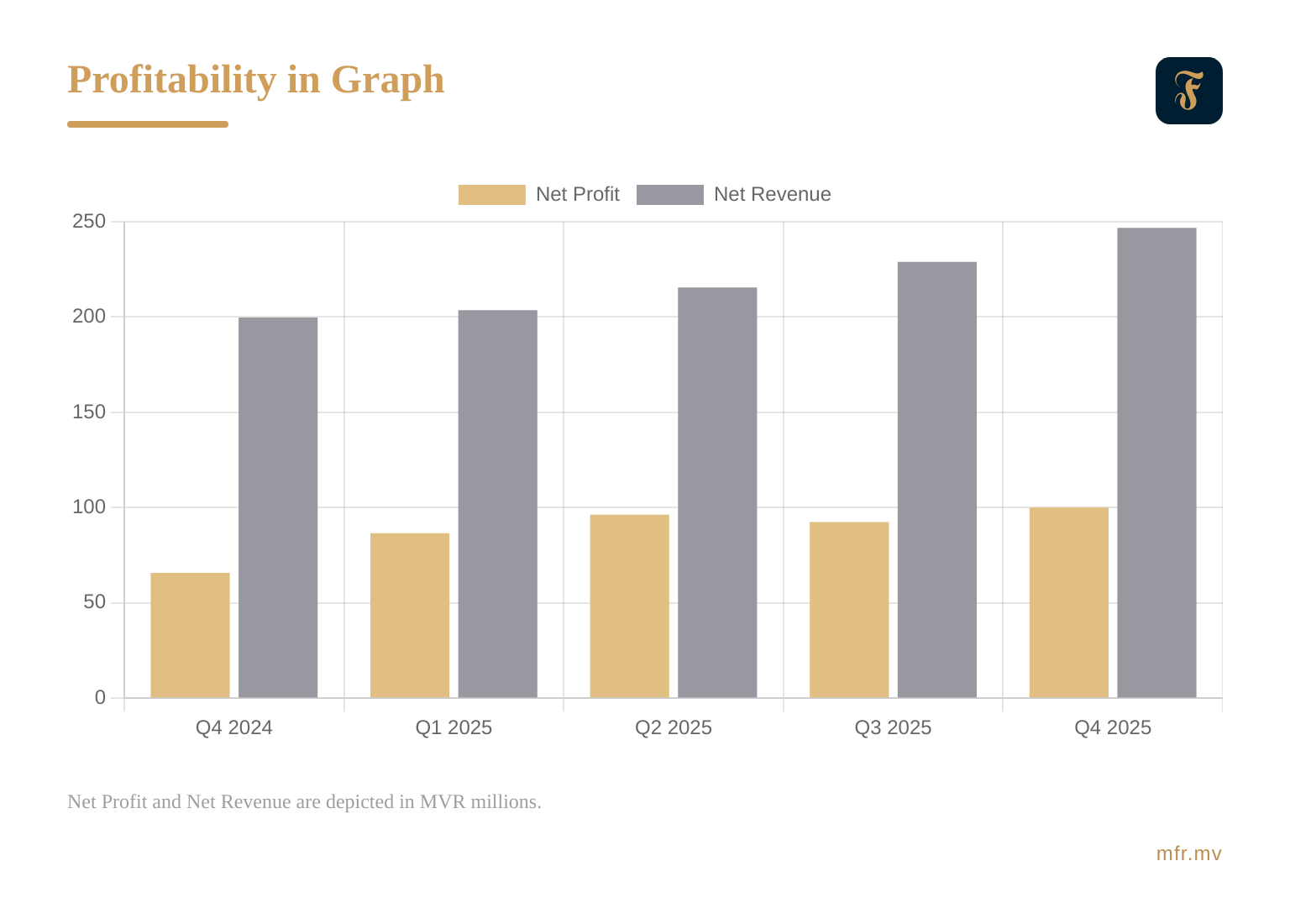

Profitability

Profitability strengthened further in the fourth quarter as revenue growth continued to support earnings expansion. Total revenue rose to MVR 246.8 million, increasing 7.8% from the previous quarter and 23.5% year-on-year, reflecting growth in financing activity and fee-based income. Net profit for the quarter reached MVR 100.0 million, up 8.3% quarter-on-quarter and 52.1% compared to Q4 2024, bringing total profit for 2025 to MVR 375.4 million. Profitability ratios remained healthy despite rapid balance sheet expansion, with return on assets at 2.5% and return on equity improving to 28.1%, indicating that profitability remained resilient even as the Bank expanded its balance sheet at a rapid pace.

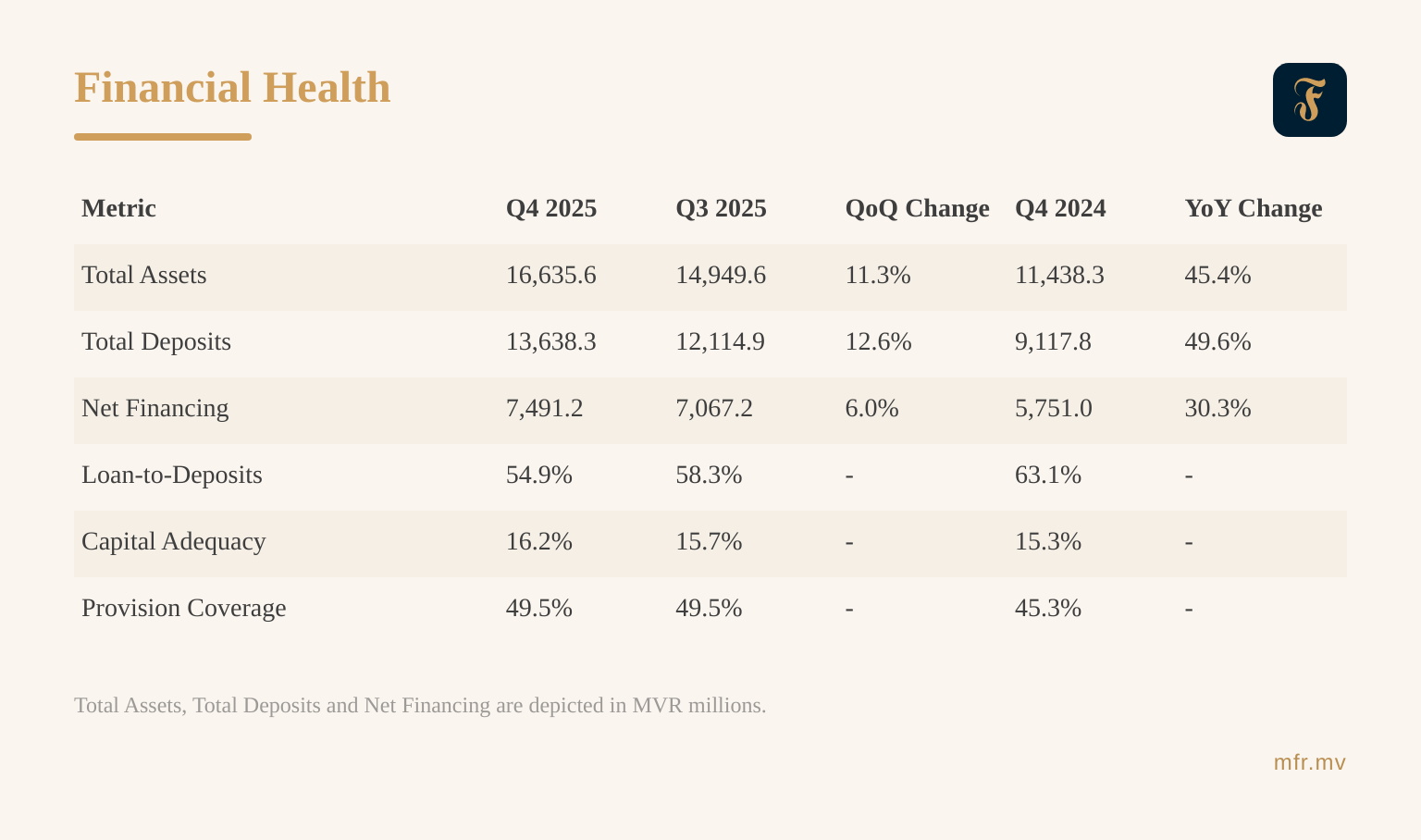

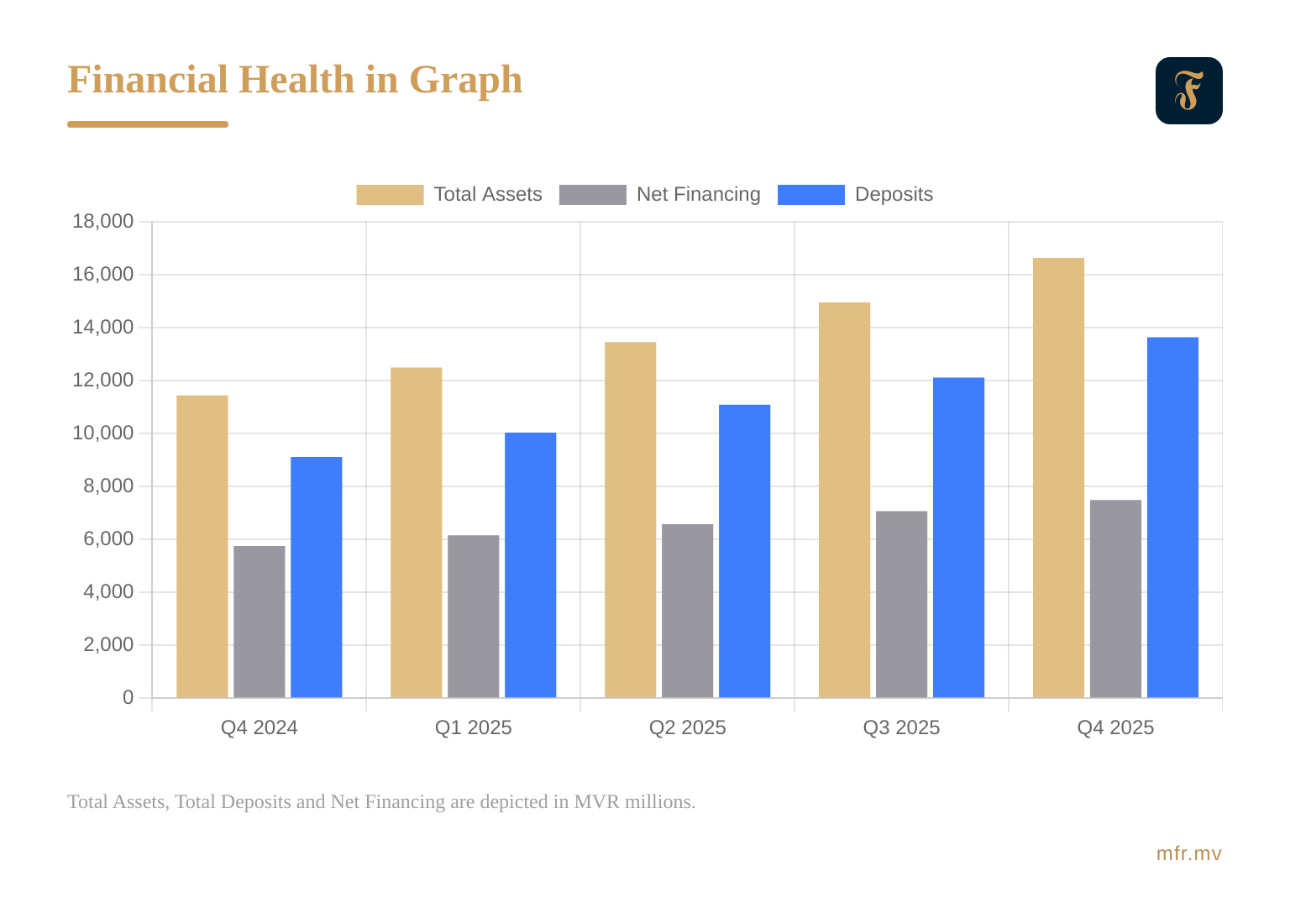

Financial Health

The Bank’s balance sheet continued to expand strongly during the quarter, supported by sustained deposit inflows. Funding growth significantly outpaced financing expansion, pushing the loan-to-deposit ratio down to 54.9%, compared with 58.3% in the previous quarter and 63.1% a year earlier, leaving the Bank with ample liquidity to support future credit growth. While net financing rose to MVR 7.49 billion, the comparatively slower pace of financing growth suggests a measured approach to portfolio expansion despite the rapid growth in deposits. Capital buffers also improved modestly, with capital adequacy increasing to 16.2%, while the provision coverage ratio remained stable at 49.5%, reflecting continued prudence in credit risk provisioning alongside the Bank’s balance sheet growth.

Valuation

Valuation multiples declined during the quarter as strong earnings growth was not matched by movements in the Bank’s share price. While profitability expanded significantly during the year, the average share price remained broadly stable at MVR 102.0, down 5.1% from the previous quarter and slightly below MVR 102.7 in Q4 2024. As a result, valuation metrics compressed materially, with the price-to-earnings ratio falling to 6.5 from 7.6 in Q3 2025 and 8.2 a year earlier, while the price-to-book ratio declined to 1.7 from 1.9 in the previous quarter and 2.0 in Q4 2024. Despite the lower multiples, the Bank continues to generate strong shareholder returns, with ROE at 28.1%, implying that the current valuation appears relatively modest compared with the Bank’s underlying profitability.

The Bank continued expanding its nationwide service delivery network during the quarter with the opening of nine new service centers across the country, further improving customer access to its banking services. MIB also introduced a POS Receivables Financing facility targeted at merchants using MIB POS terminals, enabling businesses to access working capital financing linked to their POS receivables. Operational activity continued to strengthen alongside these initiatives, with internet and mobile banking transactions rising to 22.5 million in Q4 2025, up 21.4% from the previous quarter, while card transactions increased to 3.1 million, reflecting continued growth in digital banking usage and electronic payments.

Economic conditions in the Maldives remained supportive for banking sector activity, underpinned by strong tourism performance and continued credit expansion. Real GDP grew 8.6% year-on-year in Q3 2025, reflecting sustained momentum in tourism and related sectors, while tourist arrivals increased by 10% during 2025, supporting foreign exchange inflows and domestic economic activity. Credit to the private sector also expanded, growing 13% year-on-year, indicating strengthening lending activity across the banking system. Meanwhile, inflation remained subdued at 0.4% in December 2025, helping maintain stable financing conditions.

Maldives Islamic Bank PLC is listed on the Maldives Stock Exchange under the ticker MIB, offering investors exposure to the country’s only fully Shari’ah-compliant commercial bank. 20.4% of the Bank’s share capital is publicly held, with the remaining shares owned by strategic shareholders including the Islamic Corporation for the Development of the Private Sector (ICD), and the Government of Maldives. Financial statements, quarterly reports and other corporate disclosures are available through the Capital Market Development Authority and the Bank’s official website.

This report is based on publicly available information from Maldives Islamic Bank PLC and the Maldives Monetary Authority; certain metrics presented may differ from published figures due to variations in calculation methodology.